You're at the checkout. The card is in your hand. Two versions of you are present in that moment. Present you wants to make the purchase. Future you needs the mortgage to clear next week, the utilities to clear the week after, the car payment to clear the week after that. Your conventional debit card only listens to present you.

That's because it asks only one question at the point of sale: is there enough money in the account? It's a binary query. The card (and the system it belongs to) doesn't track what the money is for, what's already promised, or what bills are coming up. If the balance is positive, the transaction clears, and you’re left to fend for the future.

The authorization layer doesn't read spreadsheets. It reads the balance and approves.

This is the gap that mental organization can't close. You might have separated your money in a spreadsheet, opened multiple accounts to mimic envelopes, or set caps in a budgeting app. None of that survives the point of sale. The authorization layer doesn't read spreadsheets. It reads the balance and approves.

Behavioral research has long pointed to why this is so hard. In a landmark study, Hal Hershfield and colleagues at Stanford showed participants age-progressed images of themselves before asking how much of their pay they wanted to put toward retirement. The participants who saw their future selves allocated about 30% more than those who didn't. The presence of the future self changed the present decision. When future you is visible at the moment of choice, present you makes better decisions for both.

Richard Thaler and Shlomo Benartzi found a second way to bring future you into the decision: stop depending on the moment of choice. Their Save More Tomorrow [LINK: https://www.shlomobenartzi.com/save-more-tomorrow] program asked workers to commit a share of their future raises to retirement before the money ever reached them, and millions saved more as a result. The lesson runs past retirement. As Benartzi puts it, the design works "by taking our mental weaknesses into account," so the structure carries the weight that willpower drops at the register. Decide once, ahead of time, and the decision still holds when the card is in your hand.

When you swipe, the system knows which account to pull from and which ones are spoken for. It's non-destructive authorization because present you can't hurt future you.

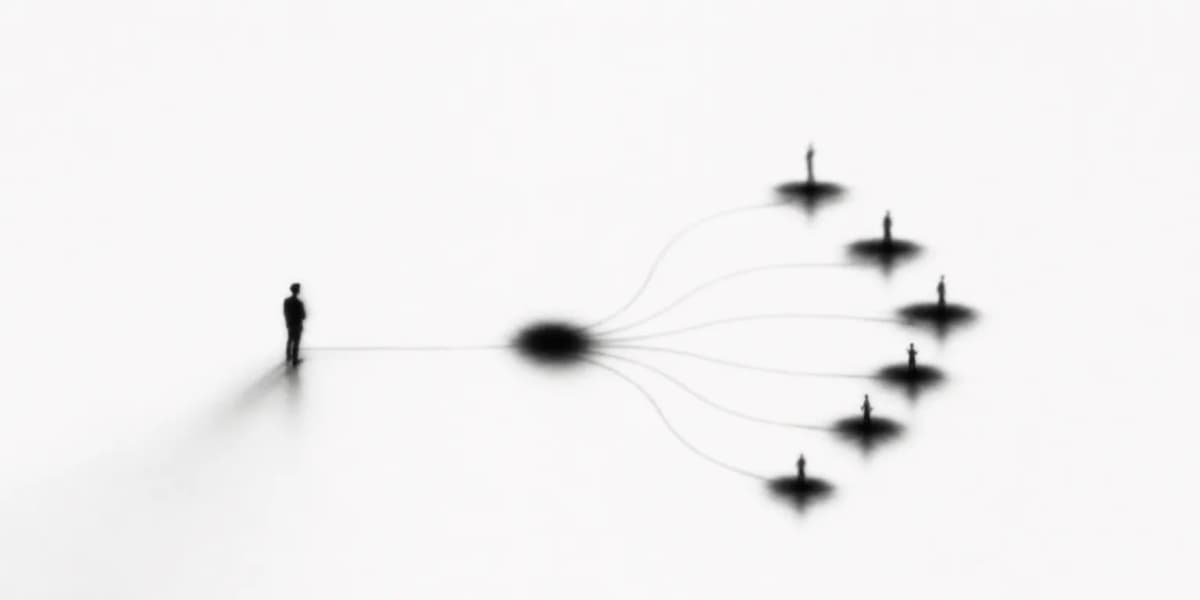

The Magnitude debit card carries that same idea into every transaction. Behind the card is Reserve Rails, the architecture that sorts your money into purpose-bound reserves the moment your paycheck lands. [CROSS-LINK: Direct deposit delight] Housing has its own account. Utilities. Groceries. When you swipe, the system knows which account to pull from and which ones are spoken for. It's non-destructive authorization because present you can't hurt future you.

The old mechanics were destructive. With a traditional card, your balance showed a sum of $2.5k. Every swipe cleared because all the money was lumped together.

The new mechanics are non-destructive. With a Magnitude debit card, you have distinct balances that add up to $2.5k. Each swipe clears because the money has purpose.

When the authorization knows the structure, the swipe stops being a moment present you decides alone. Future you is already at the checkout, holding the bills that have to clear next week. The system represents both of you. Today's transaction can go through without putting tomorrow's commitments at risk.

A typical card asks "Can you spend it?" The Magnitude card asks "Can you safely spend it?"

A typical card asks "Can you spend it?" The Magnitude card asks "Can you safely spend it?" Both questions can clear the same swipe. Only one keeps the rest of the month intact. That's what non-destructive authorization means.

Protecting tomorrow also returns something to today. Because Magnitude operates upstream of the payment network, the value the system creates flows back in the form of an annual rebate for all Magnitude members. This can be hundreds of dollars a year–much more than your annual membership.

Sources.

-

Hershfield, H. E., Goldstein, D. G., Sharpe, W. F., Fox, J., Yeykelis, L., Carstensen, L. L., & Bailenson, J. N. (2011). Increasing saving behavior through age-progressed renderings of the future self. Journal of Marketing Research, 48(SPL), S23–S37. journals.sagepub.com/doi/10.1509/jmkr.48.SPL.S23

-

Thaler, R. H., & Benartzi, S. (2004). Save More Tomorrow™: Using behavioral economics to increase employee saving. Journal of Political Economy, 112(S1), S164–S187. Save More Tomorrow