Most people don't switch traditional banks. Americans keep the same checking account for 19 years on average, and 43% say they stick with their current bank because it's what they've always had, or it would be too much of a pain to switch.

So, you stay put.

But that means the interface stays bad. The picture of your money stays cloudy. You keep guessing at the end of every month whether you came out ahead or behind.

On the other hand, there's a new wave of people—fed up with traditional banks and looking for alternatives—switching to neobanks like Chime, Borrow, and Revolut. These new options might offer flashier interfaces or user experiences, but underneath they're no different from what people left behind.

All these banks are interchangeable. They hold your money and report a balance. If they have 100 features, 99% of them are the same. There's very little difference between them. And there's a reason. They all operate in the smog of a single balance.

Magnitude turns the one-balance bank account into multiple reserves that all have a distinct purpose.

Magnitude does something unique: multiple balances. We call it high-altitude banking because everything gets its own oxygen supply. Built on a new primitive, Reserve Rails, Magnitude turns the one-balance bank account into multiple reserves that all have a distinct purpose.

Here's what it looks like.

Day one. You download the app from the App Store. Either become a Magnitude member with a personal, couple, or family membership, or continue with the setup before you decide to join, like try before you buy. Just by moving through the setup process, you'll already be able to see your annual rebate based on your monthly spending. [CROSS-LINK: The math.] You can use your iPhone by itself, but Magnitude works across the Apple ecosystem when you link your Apple Watch or iPad. You enter one number, your projected annual income, and the whole system comes alive around it. If at this point you signed up for a membership, your physical debit card is on its way to you via expedited shipping. Couples each get their own card. If you didn't get a membership, you're free to keep going in the setup process.

Day two: Even before you sign up for a membership, Magnitude shows you what people near you spend on groceries, utilities, housing, transportation, and other recurring expenses. For example, you tap groceries and see that the local median is $620 a month. You keep that amount, or change it, and once you have a membership, Magnitude will fund that account from your income when your next paycheck lands. Advanced users can add sub-accounts, even merchant-specific ones for Apple, Amazon, AAA, or Costco.

Magnitude's 85% default is built around what's actually happening, not what a budgeting app wishes were happening.

Day three. You confirm your payday frequency and customize your allocations. [CROSS-LINK: Direct Deposit Delight] The default is 85% to needs like housing, insurance, car, utilities, and subscriptions. That's because the typical household spends roughly 80% of what they earn on the same kinds of essentials, according to Bureau of Labor Statistics data. Magnitude's 85% default is built around what's actually happening, not what a budgeting app wishes were happening. What's left, 15%, splits evenly into discretionary spend: wants, goals, and investing (until you customize it).

Day four: By now, you're getting the big picture and seeing the value of Magnitude, so you sign up for either an annual or lifetime membership. The moment you join, go and check your enjoy account balance for a little something on us. Your Magnitude debit card is on its way via expedited shipping. Couples get two.

Day five. Use your enjoy account to treat yourself to something nice. A coffee. Lunch. A pair of movie tickets. You're now experiencing how Magnitude works on a small scale, without having committed a single paycheck.

Day six. Now it's time to point your direct deposit at Magnitude. We make it easy. You can do this directly in the Magnitude app by following step-by-step instructions. Or you can email yourself a PDF that you can give to your employer or HR department.

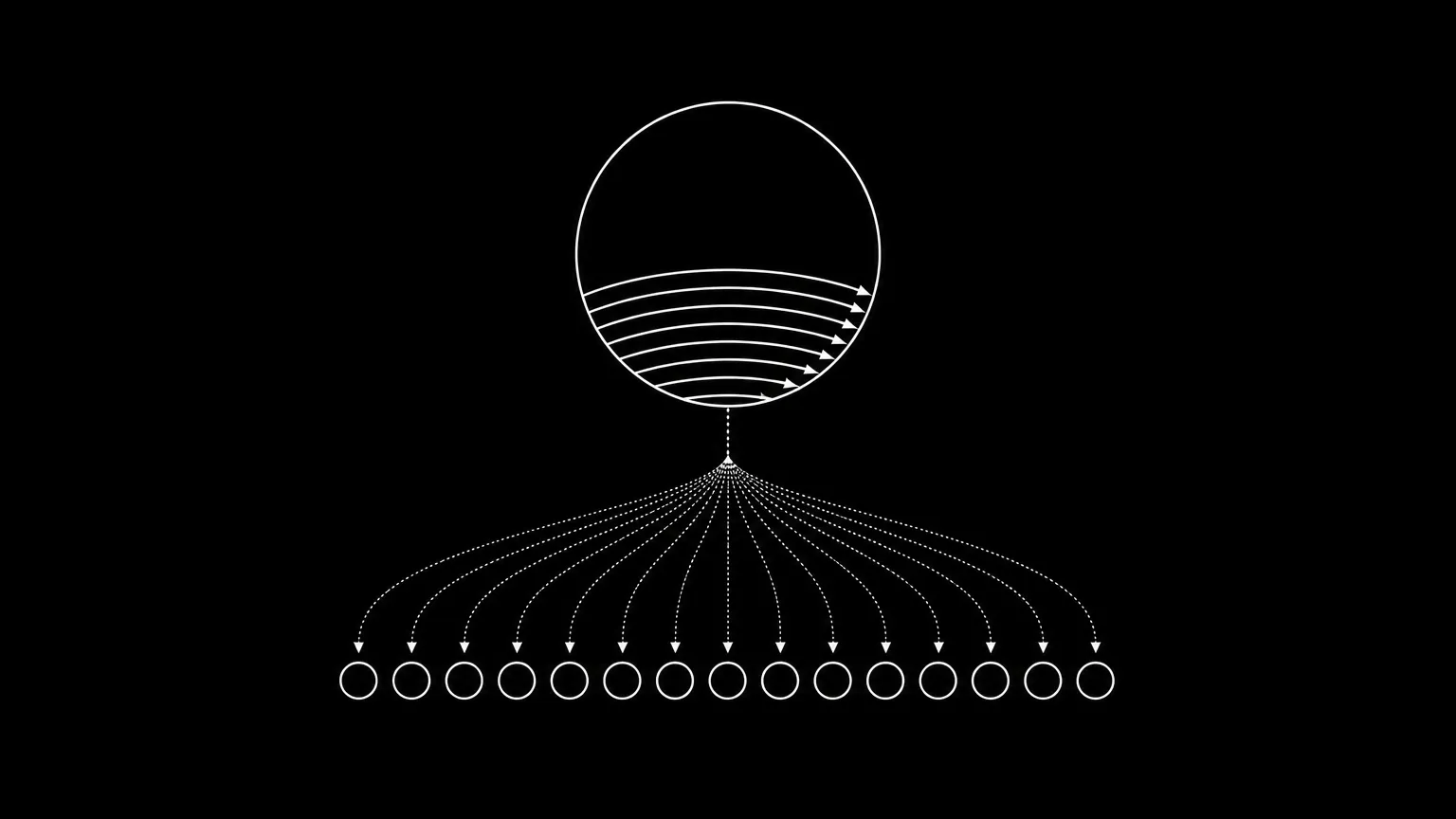

Day seven. Your physical debit card arrives. You open the app, create a four-digit PIN, and tap to link it. That new black card in your wallet now pulls from up to 15 expense accounts and one spending (enjoy) account, all with their own dedicated account numbers. [CROSS-LINK: The non-destructive authorization.] Now, when you spend, you can just use your physical Magnitude debit card, or you can set it up with Apple Pay on your iPhone—your choice.

When your first paycheck lands in Magnitude, you have what no traditional bank account has ever given you: a clear picture of where your money is, where it's going, and what's already been handled.

When your first paycheck lands in Magnitude, you have what no traditional bank account has ever given you: a clear picture of where your money is, where it's going, and what's already been handled. Change a default whenever you want and it takes effect on the next paycheck. Nothing is locked in. Everything is visible.

A traditional bank holds your money and reports a balance. Magnitude runs your money the way you'd run it yourself—if you had the time, the spreadsheets, and the foresight. A week is enough to feel the difference. After that, going back to a balance and a guess feels like flying with the instruments turned off.

You don't have to imagine how your money should feel. Give it a week, and you'll know.

Sources

-

Karen Bennett, "Survey: Many consumers stick with same bank accounts for decades, cite convenience as a factor," Bankrate, March 10, 2025.

-

US Bureau of Labor Statistics, "Consumer Expenditures — 2024," September 2025.

-

"Reserve Rails: Capacity, sequence, and the structural inversion of consumer finance," Magnitude.