In pre-revolutionary France, society was sorted into three estates. The First Estate was the clergy. The Second was the nobility. The Third was everyone else: the farmers, the merchants, the laboring families. The first two estates owned most of the land, held most of the wealth, and paid almost none of the taxes. The Third Estate did the work, paid most of the taxes, and absorbed the cost of every bad harvest, war, and royal decision. The estates were abolished in 1789. The pattern they built didn’t fully go with them.

You can see that pattern again, two and a half centuries later, in modern household finance.

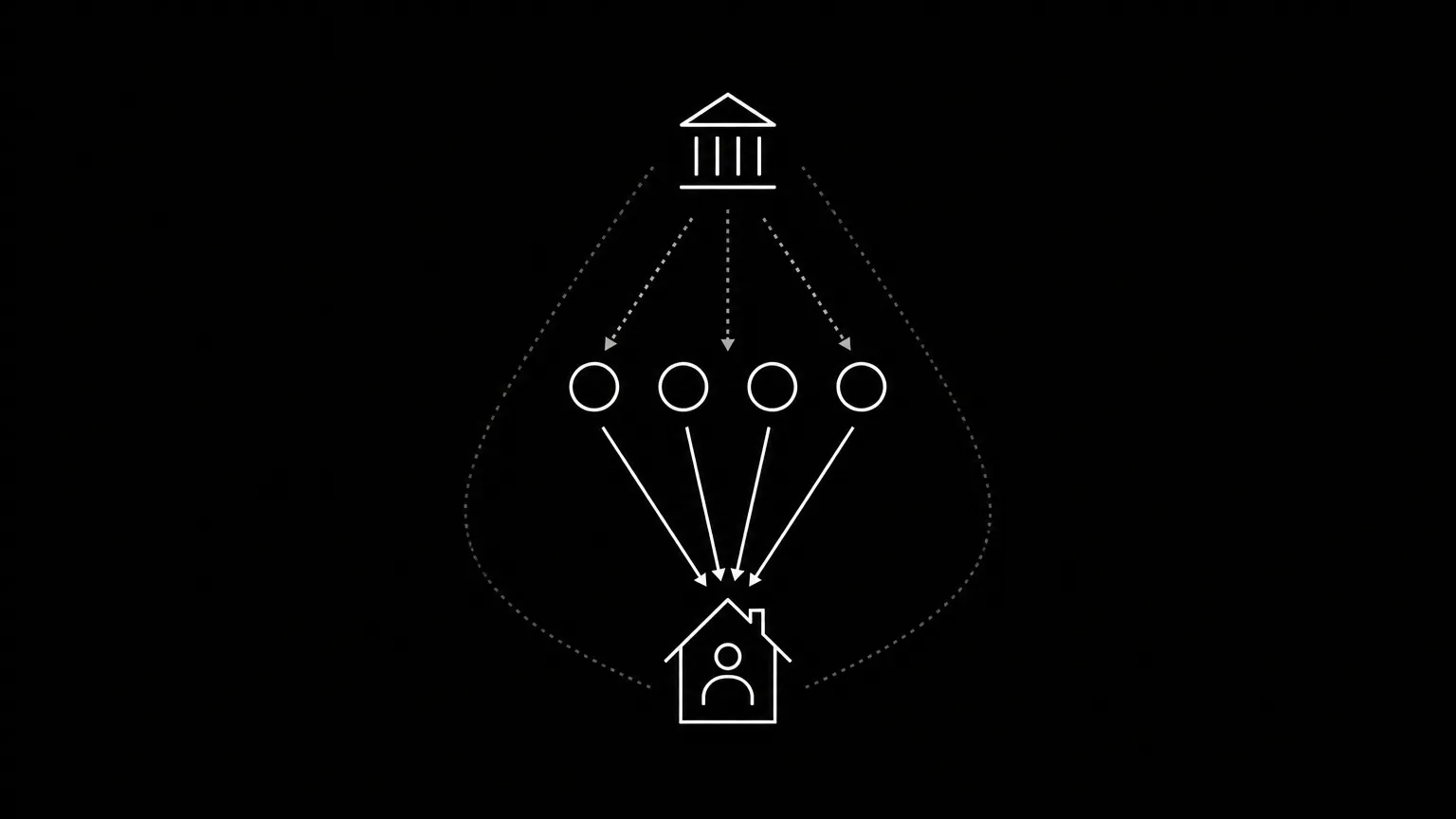

The First Estate today is your bank. The clergy ran the records of who was who. Banks run the records of who has what. They decide what counts as authorized, when transactions clear, and what the balance reads at any given moment. Regulators set the outer limits, but the operational power lives inside the bank. The whole system passes through them because that’s how it was built.

The Second Estate today is everyone who profits from what banks don’t do well. The nobility collected rents, tolls, and fees from anyone who passed through their land. Credit card companies collect interest from anyone who can’t pay in full. Buy-now-pay-later lenders collect fees from anyone who needs to spread a payment. None of them are villains. They exist because banking on its own can’t keep a household budget intact. If it could, this tier wouldn’t exist.

The Third Estate today is the household. In 1789, commoners paid most of the taxes, ate the loss when grain prices rose, and had no say in the laws that governed them. Households today carry the modern equivalent: the fees, the interest, the overdrafts, the late charges. They eat the loss when an unexpected bill arrives at the wrong time. They have no real leverage over the architecture that decides how their money moves. The pressure most people feel about money is positional. They’re standing in the place where the system pushes its instability down.

Households now live in real time, on infrastructure that doesn’t... They have the economic sophistication of the 21st century and the financial infrastructure of the 18th century.

The monarchy held the whole structure together by preserving the architecture. The single-balance banking model does the same job today: one pile of money, one number on the screen, infinite obligations pulling against it. The architecture was designed before real-time coordination existed, and it has stayed roughly the same while everything around it changed. Households now live in real time, on infrastructure that doesn’t.

The interesting historical fact about 1789 is that the revolution was driven by a structure that no longer matched the country it was meant to govern. The moral arguments came after. The same kind of mismatch is showing up now, in a different domain. Modern households have the economic sophistication of the 21st century and the financial infrastructure of the 18th century.

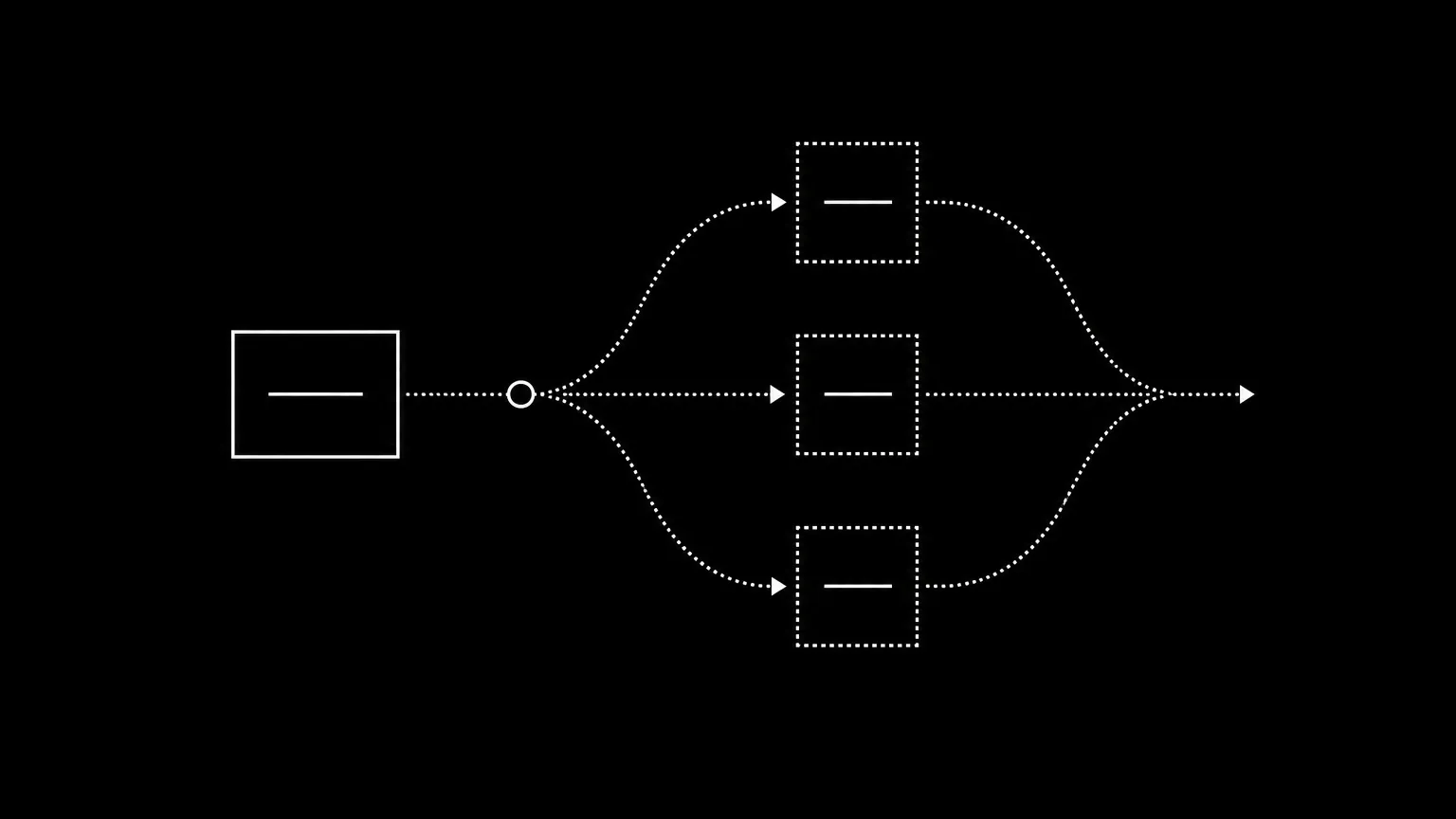

The fix lives at the level of architecture. Magnitude built that architecture and gave it a name: Reserve Rails. Other tools let households move money into multiple accounts manually, after the fact, but managing them just makes for a lot more work. [CROSS-LINK: From envelopes to infrastructure.] And these separate accounts have no knowledge of one another — all they have is the ledger entry. Reserve Rails sorts money automatically into purpose-bound reserves the moment income lands, and authorizes each transaction against the right reserve. The single balance stops being the thing that decides what the household can do. Money gains direction immediately.

In revolutionary France after the abolition of the estate-based government, the instability that the Third Estate previously absorbed now got absorbed by the system. With modern finance and Reserve Rails, the instability that households used to absorb also gets absorbed by the system instead.

Reserve rails is the revolution consumer finance has been waiting for. Magnitude is the one building it.

Reserve Rails is the revolution consumer finance has been waiting for. Magnitude is the one building it. The work happens upstream of the ledger balance, on the layer that decides where money goes before the payment card network even authorizes the transaction. This means that an entirely new economic model is possible on today’s infrastructure — without rebuilding the rails. Since the payment network is ubiquitous, Magnitude works for any household at any income, immediately. And since using Reserve Rails creates enterprise value, users share in the economic upside. [CROSS-LINK: The math.] Spending $2.5k–$10k a month on regular expenses through Magnitude pays an annual rebate of $225–$900, respectively.

Reserve Rails does for money what the revolution did for power: it puts coordination in the hands of the household instead of leaving it as a privilege of the layers above.

The French Revolution abolished the estates and pushed power down toward the people who bore the burden. Personal finance is approaching the same correction. Reserve Rails does for money what the revolution did for power: it puts coordination in the hands of the household instead of leaving it as a privilege of the layers above. The rails that ring you up, now bring you up.

The quieter lesson of 1789 is that entrenched systems rarely fall outright. They get built around. The card networks aren't going anywhere, and they don't need to: Reserve Rails runs upstream of them, which makes a new economic model possible on today's infrastructure and puts it within reach of any household, at any income, immediately. No barricades required. Changing where your paycheck lands is enough.