You toggle between two apps to make one decision. The banking app shows the balance. The budgeting app shows where last month's money went. Together, they should give you what you need. But they don't. You close them both. The question you had when you opened them is still unanswered, waiting for you to do the math in your head.

Here's what's actually going on. Almost every personal finance tool you've ever used is either active or passive. Banks are active. They let you operate your money by moving funds, paying bills, and transferring money. Budgeting apps are passive. [CROSS-LINK: Exhausting.] They let you observe your money by categorizing, labeling, and summarizing what you've already spent. One glance at the app store and it's easy to see that there are hundreds of each—and they're essentially all the same.

These states—operational and observational—do useful work on their own. Operational tools get money where it needs to go in the moment. Observational tools tell you what happened with the money after the fact. Both are necessary. Neither one structures the money before the next decision arrives.

The number on the screen is accurate, but incomplete: budgets don't often survive past the point of sale. It leaves the hardest work to you.

No matter which app you open first, you have to figure out what to do every single time. You're standing at the checkout, looking at a balance that knows the size of your account but not the shape of your month. The number on the screen is accurate, but incomplete: budgets don't often survive past the point of sale. It leaves the hardest work to you, deciding whether the size is enough for everything that's coming.

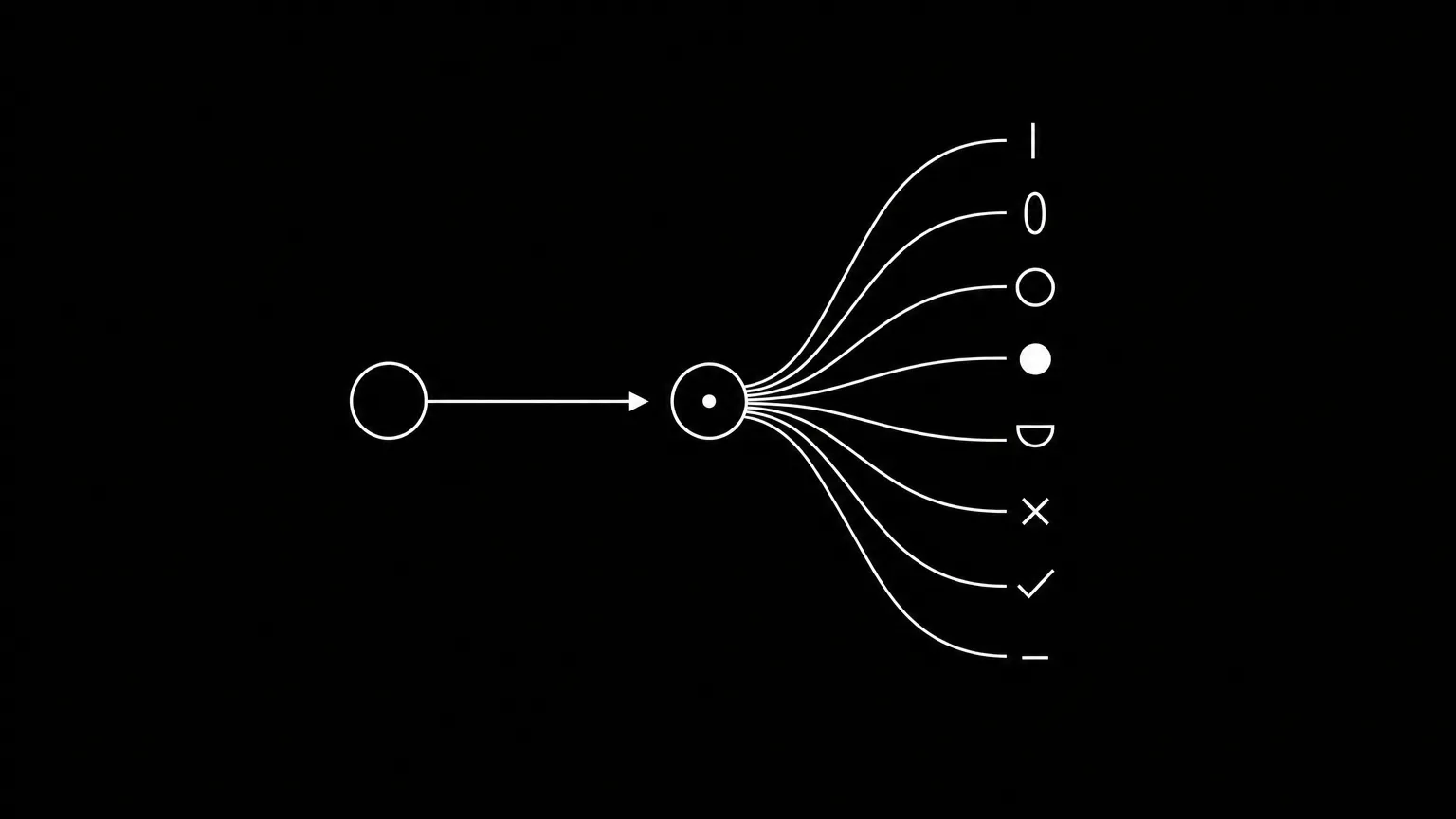

So, what are the states of operation (banking) and observation (budgeting) missing? Coordination (routing). With coordination, each obligation is proactively funded the moment your paycheck lands. Money is routed to where it needs to go without you having to tell it every time. The routine work of pointing dollars at the right things gets handled by the system, in real time, without you having to remember.

Think about driving. The rearview mirror shows where you've been. The steering wheel lets you change direction. Both useful, both vital. But the route—the part that knows which turns are coming and when—is set before you put the car in motion. The driving and the watching get easier because the path was coordinated first.

Money should work the same way. The moment income arrives, every dollar should already know where it's being routed. [CROSS-LINK: From envelopes to infrastructure.] Housing has its place. Utilities have theirs. Groceries. Savings. A buffer for the unexpected. Each holds its position before any decision pulls against it.

Once the coordination state is in place, operation and observation don't go away. They just stop being your job to figure out.

Magnitude introduces the coordination state to personal finance. It resolves a missing dimension so needs are anticipated and money responds as things change. Once the coordination state is in place, operation and observation don't go away. They just stop being your job to figure out. Separate banking and budgeting apps stop being necessary–they're both built into Magnitude itself.

The most important decisions about your money are made in Magnitude the moment your paycheck lands. The relief comes from being free to make all the big decisions once. The smaller decisions feel good because you know they're aligned with what you really want: to spend less energy figuring out money, so you can invest more energy in figuring out life.