Overspending is the guilt trip the financial world leaves you with when the numbers don’t line up. It suggests a discipline problem. A character flaw. Moments of weakness that can be fixed with better willpower. It isn’t any of those things. Overspending is a timing problem masquerading as a spending problem.

Here’s how it plays out. Let's say your paycheck lands on a Friday. You spend money on the things you want right away. Shoes, dinner, concert tickets. Three days later, rent posts. The utility bill clears on the 15th. The car payment lines up with the 20th. You didn’t necessarily buy more than you earned this pay period. You just let a want clear before a need. By the time the need arrives, the balance is smaller than it should be, and your account takes the hit. From the outside in, it looks like you spent too much. From the inside out, it feels like you never have enough.

Self-doubt at least gives you something to fix: try harder, spend less, pay closer attention. The alternative is harder to see.

The instinct is to blame yourself. It seems like simple math: if the account is short, you must have spent too much. If you're stressed, you must have gotten off track. Self-doubt at least gives you something to fix: try harder, spend less, pay closer attention. The alternative is harder to see: that the system you’re relying on was never designed to keep up with your life.

Thinking that you're the problem keeps you looking in the wrong direction. The anxiety is a result of something you can't control: the ledger itself.

More than three in four U.S. workers are paid weekly or biweekly, according to the U.S. Bureau of Labor Statistics. Meanwhile, the largest recurring bills (rent, mortgage, utilities, insurance, subscriptions) almost all occur at random times throughout the month. One balance being pulled in multiple directions. Money coming in. Balance going up. Money coming out. Balance going down. No bearings. Single point of failure. No tool can keep up with this.

It gets even more complex when you add credit into the equation. And yes, a budgeting tool can wrangle it all, but no one wants to look at it, for good reason. You know where it went.

The ledger was designed as an accounting system, not a coordinating system. The burden is on you.

All this misalignment is a structural mess. It isn’t something you can fix. Why? Because you're beholden to other schedules. Your employer picks your pay date. Your lender picks the date of your car payment. The utility company picks a date and the amount varies. Your bank just shows you a balance. This isn't helpful. The ledger was designed as an accounting system, not a coordinating system. The burden is on you. [CROSS-LINK: Timestamp vs. timeframe.]

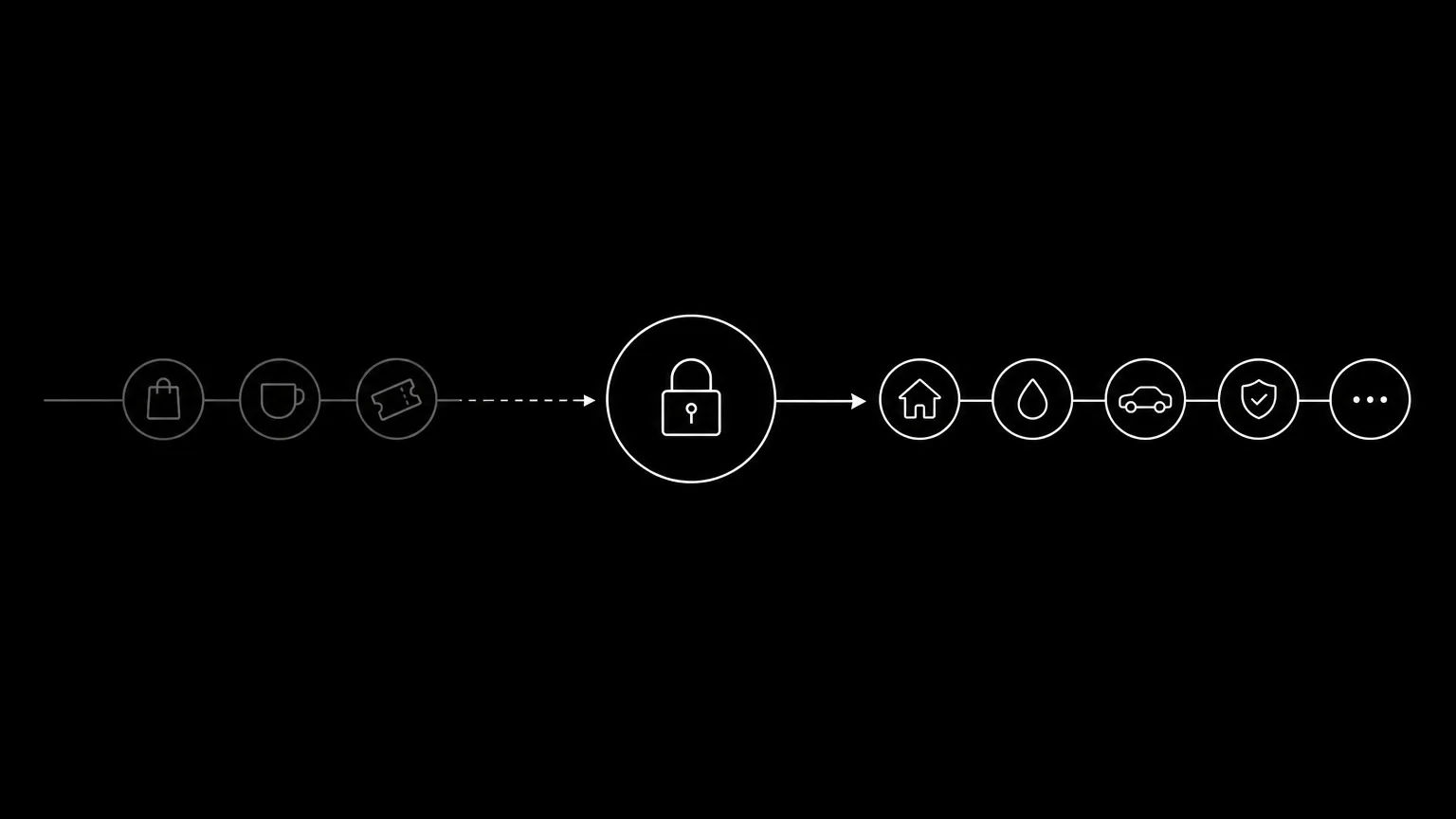

We’ve been calling it overspending for so long that it sounds unsolvable. What’s happening is a transaction is clearing in the wrong order. And there isn't a system that exists today that enforces the right sequence: needs should come before wants, every time.

So, you bought the shoes. Because the bank balance said “yes,” the card said “yes.” [CROSS-LINK: The lie of the bank balance.] Three days later, the utility bill hit the account and there wasn’t enough left. An overdraft fee landed. You get an email that says non-sufficient funds (NSF). But that wasn't overspending. Your bank just isn't capable of sequencing.

The fix doesn’t start with spending less. It starts with needs being protected before any want can reach them

That’s a timing gap, not a discipline gap. The fix doesn’t start with spending less. It starts with needs being protected before any want can reach them—with the money arriving in the right order, without having to reconstruct the order in your head with every purchase.

When that cognitive load disappears, the pressure does, too. Because the stress wasn’t about the money. It was about the mental math we were doing every day. Give that job to the right system and the math falls quiet. The shoes start feeling affordable. The concert tickets stop feeling like a splurge. Now that your rent is covered, shopping feels good again. None of this has to be held in your head, ever again.

Here’s the conundrum. Banks reconcile their own income and expenses every day. Commercial banking products routinely include cash-flow forecasting, AP/AR reconciliation, and treasury management. The consumer is a party to the system but only to the benefit of the bank. If the bank were to do all these things for the customer, its incentive structure would collapse.

Sources.

- U.S. Bureau of Labor Statistics. Length of pay period in the Current Employment Statistics survey. bls.gov/ces/publications/length-of-pay-period.htm [TO VERIFY at draft lock — confirm latest release year and exact pay-frequency percentages before publish.]