Long before fintech, households had already figured out something important about money: it works better when each dollar is assigned a purpose before it's spent.

For much of the 20th century, that logic often showed up in envelopes. A paycheck came in. Cash was split into categories like housing, groceries, utilities, savings, and other needs. The money for each obligation was separated before the next decision had to be made.

Paper wasn't the insight. Process was the insight. Allocation happened as soon as income arrived–way before money was spent.

Households were doing something structurally right. They were making decisions upstream, while the money was still intact, instead of waiting until the end of the month to interpret the damage. The budget wasn't a report. It was already embodied in the arrangement of the money itself.

The envelope created a boundary. And the boundary was the point. What people now call discipline was often just structure.

That mattered because financial pressure changes decisions. A dollar sitting in a generic pile is easier to rationalize away than a dollar already assigned to rent. The envelope created a boundary. And the boundary was the point.

What people now call discipline was often just structure. This is the part modern finance forgot. As the world became digital, the envelope system became harder to maintain by hand. Income moved electronically. Bills became automatic. Cards replaced cash. Households accumulated subscriptions, annual renewals, shared accounts, variable expenses, and a faster rhythm of spending. The old logic still worked. But the manual version of it stopped scaling.

Households were left with a choice: keep carrying the model themselves, or fall back to a checking account and try to remember everything in their heads.

That was the downgrade.

The enterprise got Enterprise Resource Planning (ERP). The household got a checking account. That's the asymmetry.

Because while households lost the operating logic, institutions gained it. The same pre-allocation instinct that households practiced informally was later formalized in other domains. Zero-based budgeting gave organizations a more explicit way to assign resources on purpose rather than letting spending drift from prior assumptions. Then enterprise software went further. Companies got systems that tied money to plans, departments, purchasing, workflows, approvals, and future commitments. Over time, the enterprise gained an operating layer for capital allocation. The household did not.

The enterprise got Enterprise Resource Planning (ERP). The household got a checking account. That's the asymmetry.

A company doesn't run its finances by staring at one number and hoping managers remember what the money is supposed to cover. [CROSS-LINK: The lie of the bank balance.] Its systems distinguish between categories of capital, committed uses, timing, approvals, and constraints. Capital isn't treated as one undifferentiated pile. It's organized before decisions are made under pressure.

Households, meanwhile, are still expected to do exactly that.

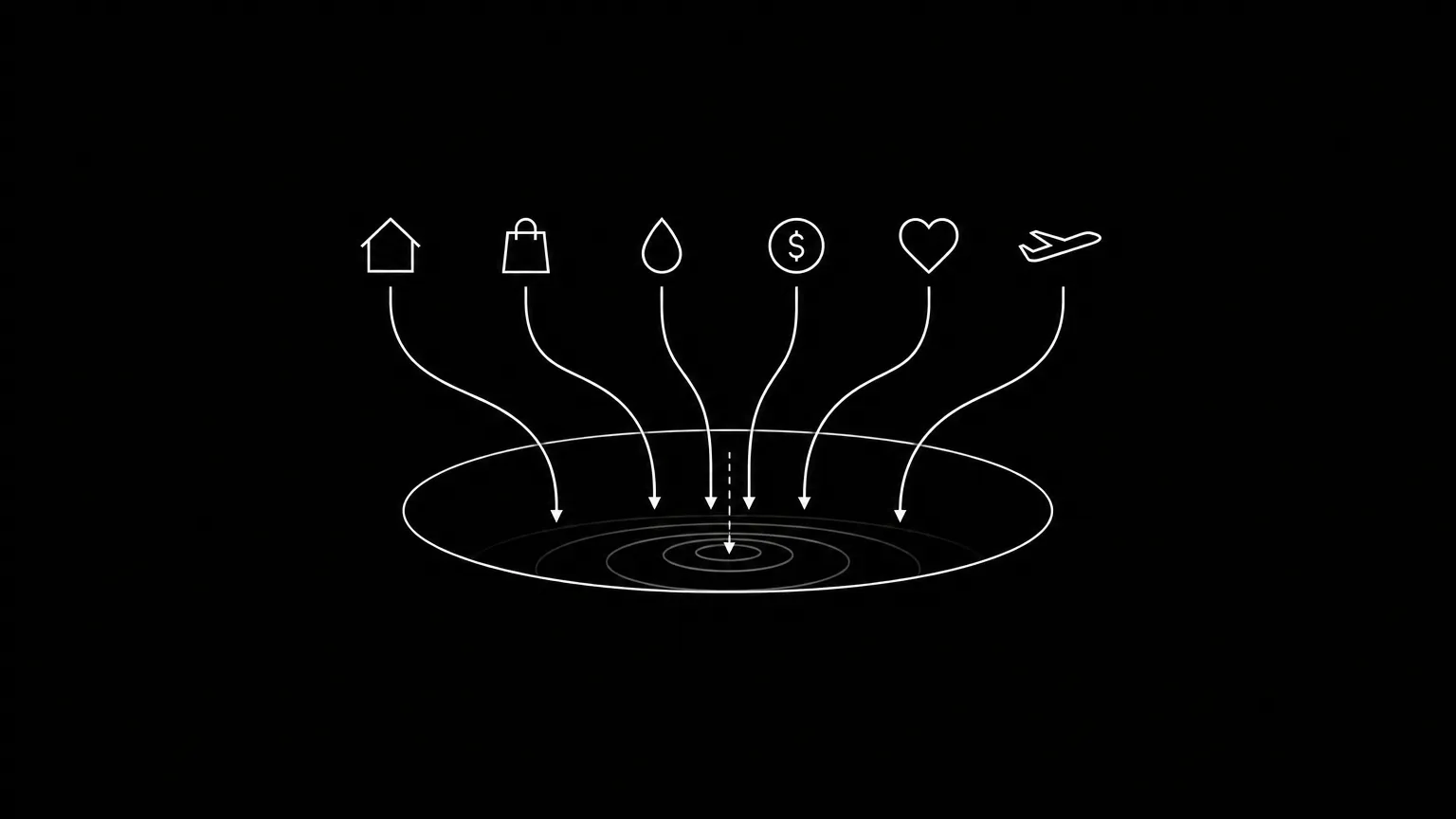

They receive income as one balance. Then they mentally divide it across housing, groceries, debt, savings, child expenses, subscriptions, annual obligations, and everything else life demands. The sequence between needs and wants still lives in memory. The future still has to be simulated by hand. And every purchase still risks pulling from the same pool of money as something more important.

That's why personal finance still feels strangely primitive. We digitized the account, but not the logic.

We gave households better interfaces, faster payments, prettier charts, and more notifications. But we didn't give them the equivalent of an operating system. We gave them visibility without structure. History without protection. Information without pre-allocation. So, the real problem was never that households lacked discipline. It was that they were left to perform system work manually.

People still patch over this gap in familiar ways. They budget after the fact. [CROSS-LINK: Exhausting.] They open multiple accounts. They move money around by hand. They build spreadsheets. They rely on credit cards to absorb timing mismatches. They create rules for themselves and then try to remember them in real time. All that points to the same problem: the underlying banking model never absorbed the job.

The missing layer is not another dashboard. It's infrastructure.

What households need is the same core advantage institutions got: a system that assigns money to purpose before it can be casually pulled from somewhere else.

What households need is the same core advantage institutions got: a system that assigns money to purpose before it can be casually pulled from somewhere else. A system that preserves commitments. A system that makes sequence visible and enforceable. A system that stops asking the brain to do what the architecture should have done.

That's what Reserve Rails are for.

Reserve Rails take the old logic of envelopes and embed it in software and infrastructure. Income is allocated on arrival, before competing demands can pull from the same dollars. Money for rent is protected before discretionary spending begins. Money for groceries stays distinct from money for travel, subscriptions, or a future goal. The point is not cleaner categorization. The point is to make money move in the right order by default, so households stop depending on memory, patchwork, and credit to hold the month together.

That's the evolution. Not from envelopes to budgets. Not from envelopes to better apps. From envelopes to infrastructure.

The household was never wrong to separate money by purpose. It was early. The mistake was leaving that logic trapped in paper, memory, and manual effort while every other domain got software. The best idea in old money management was pre-allocation. The next step is not to abandon it. The next step is to build it into the system.